Polyethylene Market Global Report with End-Use Trends and Forecast 2025–2033

Polyethylene Market Overview and Growth Outlook

According To Renub Research global polyethylene market continues to hold a central position in the plastics and petrochemicals industry due to its extensive use across packaging, construction, automotive, agriculture, and consumer goods. Polyethylene is a thermoplastic polymer produced primarily from ethylene derived from petrochemical feedstocks. Its versatility, durability, chemical resistance, and cost-effectiveness make it the most widely manufactured plastic globally. The market is segmented into major product types such as low-density polyethylene, linear low-density polyethylene, and high-density polyethylene, each offering distinct mechanical and functional properties suited to diverse applications.

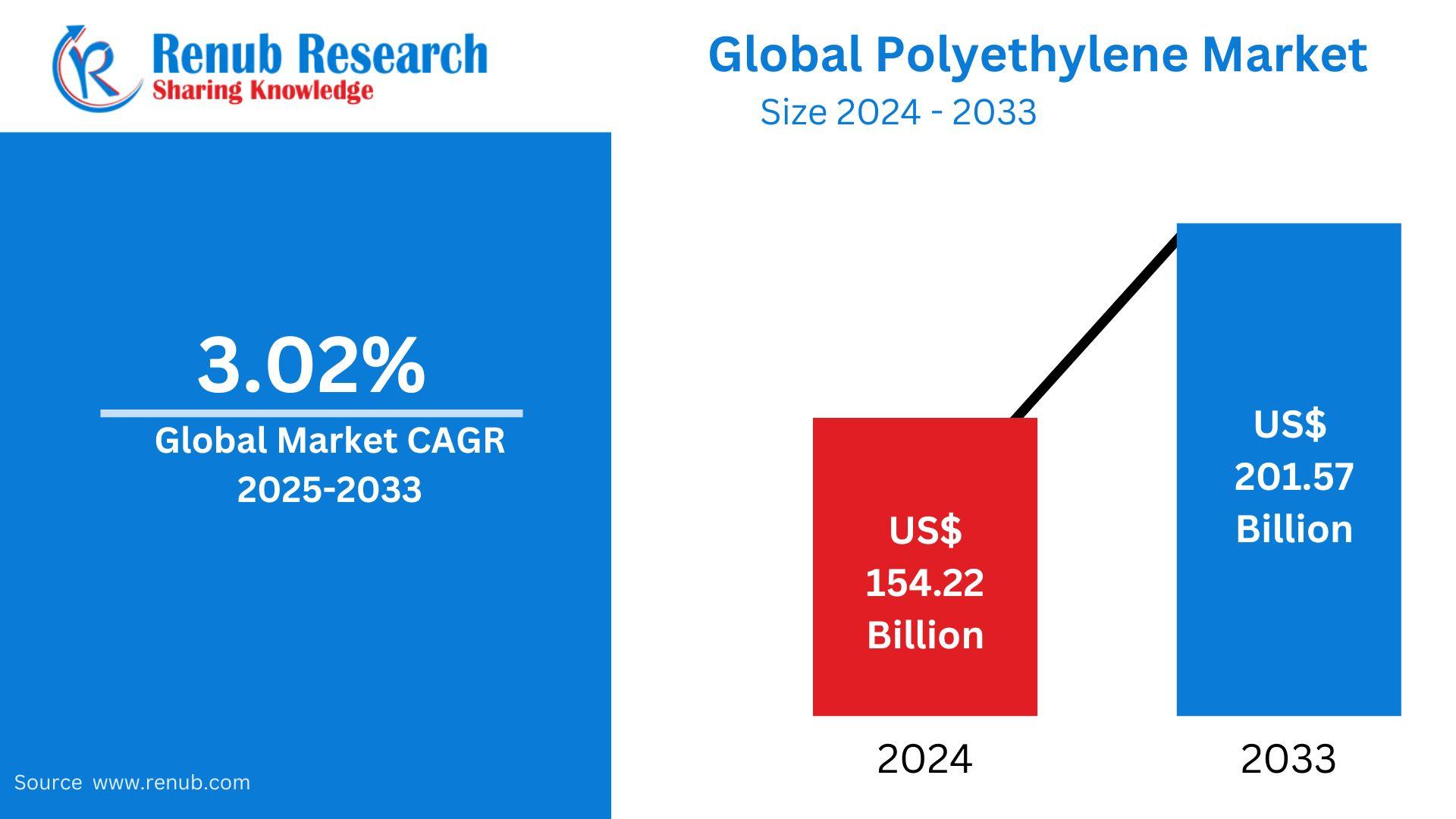

The polyethylene market is expected to expand from a valuation of US$ 154.22 billion in 2024 to approximately US$ 201.57 billion by 2033, registering a compound annual growth rate of 3.02% during the forecast period from 2025 to 2033. This steady growth is supported by rising demand for lightweight and affordable materials, continuous technological advancements in polymer processing, and strong consumption from end-use industries. Despite mounting regulatory and environmental challenges, polyethylene remains indispensable due to its adaptability and ongoing innovation in recycling and sustainable production methods.

Download Free Sample Report:https://www.renub.com/request-sample-page.php?gturl=polyethylene-market-p.php

Role of Polyethylene in the Global Packaging Industry

Packaging represents the largest and most influential end-use sector for polyethylene worldwide. The material is extensively used in flexible packaging, films, bottles, containers, bags, and protective wrapping due to its excellent moisture barrier, strength, and flexibility. As consumer lifestyles shift toward convenience-oriented products, the demand for packaged food, beverages, and ready-to-use goods continues to rise, directly fueling polyethylene consumption.

The rapid expansion of e-commerce has further amplified the need for durable yet lightweight packaging materials capable of protecting goods during transportation. Polyethylene fulfills these requirements efficiently while keeping logistics costs low. Innovations such as multilayer films, downgauging techniques, and recyclable mono-material packaging solutions have expanded polyethylene’s application scope. These developments enhance product shelf life, improve safety, and align with sustainability goals, reinforcing polyethylene’s dominance within the global packaging ecosystem.

Infrastructure Development and Construction Demand

Global infrastructure development and urban expansion play a significant role in driving polyethylene market growth. High-density polyethylene is widely used in construction applications such as pipes, fittings, insulation materials, geomembranes, and protective coatings. Its corrosion resistance, flexibility, long service life, and low maintenance requirements make it an ideal alternative to traditional materials like metal and concrete.

Developing economies are investing heavily in water management systems, gas distribution networks, telecommunications infrastructure, and urban housing projects. These initiatives significantly boost demand for polyethylene-based piping and construction materials. Additionally, the growing adoption of green building practices and smart city projects further supports polyethylene usage, as the material contributes to energy efficiency and reduced environmental impact throughout a building’s lifecycle.

Technological Advancements in Polyethylene Production

Technological innovation has significantly enhanced the performance characteristics and application range of polyethylene. Advances in catalyst technologies, particularly metallocene catalysts, have enabled manufacturers to produce polyethylene grades with superior strength, flexibility, and clarity. These improvements allow for material reduction without compromising performance, aligning with sustainability and cost-efficiency objectives.

Product innovation has also led to the development of specialty polyethylene grades designed for medical devices, high-barrier packaging, and advanced industrial applications. Furthermore, progress in polymerization processes has improved production efficiency and reduced energy consumption. The integration of digital technologies and automation in manufacturing plants has streamlined operations, enhanced quality control, and lowered operational costs, strengthening the competitiveness of polyethylene producers globally.

Emergence of Bio-Based and Recycled Polyethylene

Environmental concerns and regulatory pressure have accelerated the development of bio-based and recycled polyethylene. Bio-based polyethylene, produced from renewable feedstocks such as sugarcane ethanol, offers similar performance to conventional polyethylene while reducing carbon emissions. Although currently limited by higher production costs, advancements in bio-based technologies are improving scalability and commercial viability.

Recycling innovations, particularly chemical recycling, are transforming the polyethylene lifecycle. Chemical recycling enables the breakdown of plastic waste into its original monomers, allowing for the production of virgin-quality polyethylene from recycled materials. This approach addresses quality limitations associated with mechanical recycling and supports circular economy objectives. Growing investments in recycling infrastructure and partnerships between manufacturers and packaging companies are strengthening the long-term sustainability outlook of the polyethylene market.

Regulatory and Environmental Challenges

Despite its widespread utility, polyethylene faces increasing scrutiny due to environmental concerns related to plastic waste and pollution. Governments across the world are implementing stricter regulations, including bans on single-use plastics, mandatory recycling targets, and extended producer responsibility frameworks. These policies directly impact polyethylene demand, particularly in packaging applications.

Public perception of plastic pollution has also influenced consumer behavior, encouraging businesses to seek alternative materials or reduce plastic usage. Compliance with evolving regulations requires significant investment in sustainable product development, recycling systems, and supply chain modifications. Companies that fail to adapt risk losing market share, while proactive innovators are better positioned to navigate regulatory complexities and maintain growth momentum.

Raw Material Price Volatility and Supply Risks

The polyethylene market is highly sensitive to fluctuations in crude oil and natural gas prices, as ethylene feedstock is derived from these resources. Geopolitical tensions, production decisions by oil-exporting countries, and global energy market disruptions can significantly impact raw material availability and costs. This volatility creates challenges for manufacturers in cost forecasting, pricing strategies, and margin stability.

In recent years, energy market uncertainties have heightened supply chain risks, prompting companies to diversify feedstock sources and explore alternative production pathways. While transitioning to bio-based feedstocks offers long-term benefits, it also introduces additional complexity and capital requirements. Managing these risks remains a critical consideration for polyethylene producers operating in a dynamic global environment.

Asia-Pacific Polyethylene Market Dynamics

Asia-Pacific dominates the global polyethylene market in terms of both production and consumption. Rapid industrialization, urbanization, and population growth in countries such as China and India drive strong demand across packaging, construction, and consumer goods sectors. The region benefits from expanding manufacturing capacity, favorable government policies, and rising domestic consumption.

Large-scale investments in petrochemical infrastructure and export-oriented production have strengthened Asia-Pacific’s position in global trade. While environmental regulations are gradually tightening, the region continues to experience robust growth due to sustained economic development and increasing demand for affordable plastic products.

United States Polyethylene Market Overview

The United States polyethylene market remains one of the most technologically advanced and globally competitive. Abundant shale gas resources provide cost-effective ethylene feedstock, enabling large-scale production and export competitiveness. Key end-use sectors include packaging, construction, automotive, and consumer products.

Sustainability initiatives are reshaping market dynamics, with increased focus on recycled content and circular economy models. Investments in advanced recycling facilities and high-performance packaging solutions are supporting innovation. Major industry participants such as Exxon Mobil Corporation, LyondellBasell Industries Holdings B.V., and BASF SE continue to expand capacity and develop value-added polyethylene grades, ensuring long-term market resilience.

United Kingdom Polyethylene Market Landscape

The polyethylene market in the United Kingdom is shaped by stringent environmental regulations and strong emphasis on sustainability. Domestic production has declined over time, increasing reliance on imports to meet demand. Packaging, construction, and agriculture remain the primary application sectors, with high-density and low-density polyethylene accounting for significant market share.

Policies such as plastic packaging taxes and recycling mandates are accelerating the adoption of recycled polyethylene. Manufacturers and retailers are increasingly aligned with circular economy principles, driving innovation in recyclable and reusable packaging solutions. Despite challenges related to trade complexity and supply chain disruptions, the UK market remains stable due to regulatory clarity and consumer support for sustainable materials.

India Polyethylene Market Growth Trends

India represents one of the fastest-growing polyethylene markets globally, supported by urbanization, infrastructure development, and rising consumer demand. Packaging remains the dominant application, followed by construction, agriculture, and automotive sectors. Government initiatives such as Smart Cities Mission and Make in India are driving demand for polyethylene pipes, fittings, and industrial products.

Domestic production capacity is expanding as major players invest in new facilities and technology upgrades. While environmental regulations are evolving, the informal recycling sector plays a significant role in polyethylene reuse. With a large population and expanding middle class, India offers substantial long-term growth opportunities for polyethylene manufacturers.

United Arab Emirates Polyethylene Market Outlook

The United Arab Emirates has emerged as a strategic hub for polyethylene production and export in the Middle East. Access to low-cost feedstock, advanced petrochemical infrastructure, and favorable geographic positioning support strong export-oriented growth. Domestic demand is driven by packaging, construction, and industrial applications.

Government-led diversification initiatives and sustainability programs are encouraging innovation in recyclable and eco-friendly materials. Companies such as Borealis AG and Borouge are expanding capacity and developing advanced polyethylene grades to meet global demand. While environmental regulations are less restrictive than in Europe, increasing international pressure is pushing the market toward more sustainable practices.

Competitive Landscape and Key Market Participants

The global polyethylene market is moderately consolidated, with leading players focusing on capacity expansion, technological innovation, and sustainability initiatives. Companies compete on product quality, cost efficiency, and ability to meet regulatory and environmental requirements. Strategic partnerships, mergers, and investments in recycling technologies are common competitive strategies.

Key companies operating in the market include BASF SE, Borealis AG, Braskem, Exxon Mobil Corporation, Formosa Plastics, INEOS Group, LG Chem, LyondellBasell Industries Holdings B.V., MOL Group, and Mitsubishi Chemical Corporation. These organizations are evaluated across strategic overviews, leadership, recent developments, SWOT analysis, and revenue performance, reflecting a competitive and innovation-driven global polyethylene industry.